‘The case for Negative Emissions’ executive summary

30 Jun 2021

A call for immediate action

This report has been prepared and published to set out the research and science behind the Coalition for Negative Emissions’ view that the world is damagingly unprepared to keep to a 1.5°C pathway – in fact we find that if negative emissions solutions are not delivered at scale, even if all the 1.5°C emissions reductions pathway requirements are met, the world will break the carbon budget and exceed 1.5°C warming before 2040.

We publish this report to set the scene for a much needed, solutions-driven conversation with a wide range of global stakeholders, including academics, non-governmental organisations, industry associations, policy makers and innovators. We say ‘solutions-driven’ conversation because our hope is that a pooling of thinking through a series of workshops will push the practical development of negative emissions solutions to speedy implementation, which we see as vital to stabilising the climate alongside the current range of reductions pathways.

We look forward to your initial feedback on this report, and subsequently to engaging with you in the run up to COP26.

The full report can be downloaded at: The case for Negative Emissions.

Forewords

As the drive to combat climate change gathers pace, increasing attention is being focused on developing market mechanisms that can help achieve a pathway to net-zero. Markets are needed to establish and transmit the price signals necessary to incentivise change — for example by making emitting carbon more expensive or attracting investment into projects that will reduce or remove emissions.

Negative emissions, or removals, are a vital part of the global decarbonisation effort. The Taskforce on Scaling Voluntary Markets, with which I have been working for much of the last year, aims to mobilize a high quality, high integrity market for carbon credits with clear differentiation between neutralization (removal credits from negative emissions) and compensation (avoidance/ reduction credits). However, for the market to have a real impact we need to scale high-quality supply of negative emissions. I therefore welcome this report from the Coalition for Negative Emissions which sets out in clear and practical terms how negative emissions could be deployed on industrial scale to help the world keep global warming below 1.5 degrees Celsius.

As the Coalition argues, removal projects are a relatively small part of the market today, meaning that we are way off track in terms of delivering the necessary volume of negative emissions. The investment requirements can seem daunting, and the incentives to invest are currently weak. The Coalition is absolutely right that this state of affairs needs to change.

Part of the problem the report identifies is that the emerging carbon market does not include sufficiently clear definitions of what constitutes high-quality credits. This limits a company’s ability to invest with confidence in neutralisation or compensation. To address this issue the TSVCM is developing a set of quality standards – called the Core Carbon Principles (CCPs) – that will be finalized and curated by a Global Governance Body. This Governance Body will oversee the strategic roadmap for carbon markets, including managing the shift in the market from compensation to removal credits over time.

At the Operating Lead of the Taskforce, I am particularly excited that the Coalition members are looking to voluntary carbon markets to play an enabling role in boosting negative emissions as well as to governments to create the right incentives. An active and liquid market in both reductions and removals is needed to deliver the Paris Agreement goals. This market needs standards, and it is encouraging that the Coalition is making it a priority to ensure that negative emissions can meet the Core Carbon Principles set out in our work earlier this year.

Thus this report is an important contribution to a movement that is palpably gathering pace. We look forward to working with Coalition members and other stakeholders to make an increase in negative emissions a reality in coming years.

Annette L. Nazareth

Operating Lead for the Taskforce on Scaling Voluntary Carbon Markets Senior Counsel at Davis Polk and Former SEC Commissioner

This report is a welcome and timely contribution towards an increasingly important aspect of the climate debate. Whilst companies should clearly prioritise avoiding and minimising their emissions as part of their corporate strategies to decarbonise, we also need to be pragmatic that completely eliminating emissions will be a challenge for many organisations. The shared objective for all stakeholders in the energy transition is to ensure that organisations manage their remaining, residual emissions in a way that is transparent, credible, compatible with achieving 1.5 degrees of global warming, nature positive and just.

The World Business Council for Sustainable Development has been at the forefront of this debate for several years. Through our Natural Climate Solutions Alliance, co-chaired with the World Economic Forum, a coalition of world-leading businesses and environmental groups have come together to advocate and scale-up solutions that address the nature and climate crises together. Nature-based and Natural Climate Solutions (NCS) can remove carbon dioxide (CO2) from the atmosphere in a way that is cost-effective today while also delivering enormous benefits for biodiversity, and creating sustainable and equitable employment. Scaling these solutions in the coming years will be critical to not only fight the climate crisis, but also in promoting high-value economic ecosystems and the services they provide that we as a society rely upon, and in reversing nature loss around the world.

However, as this report highlights, to achieve 1.5 degrees of global warming we need to be pragmatic and recognise that we cannot and should not rely on NCS alone. Engineered removals, such as bioenergy with carbon capture and storage (BECCS) and direct air carbon capture and storage (DACS), will also be needed and promoting the development of a portfolio of these solutions today will give businesses and policymakers in future years greater flexibility in terms of the solutions they want to pursue. It will also enable investors and other key financial actors to make better, more informed investment decisions.

To secure buy-in from corporates, policymakers, environmental groups and the wider public, it is crucial that as these markets develop they are underpinned by rules that promote transparency and raise standards. A number of organisations are already attempting to take a leadership role to support the development of these rules, including the NCS Alliance and the Greenhouse Gas Protocol. Others are pursuing voluntary disclosure, which is also a powerful reporting tool that can help build confidence. Whatever the route, there is a genuine opportunity for businesses to take a leadership role over the coming years in raising the bar on negative emissions disclosure – particularly with negative emissions poised to be a focus area at UNFCCC COP26 later this year.

In conclusion, I warmly welcome this report. We cannot be afraid to tackle these difficult issues, which will challenge us all to reach beyond our comfort zone. We also should not overlook the significant opportunity that negative emissions presents to support prosperity and economic growth around the world by creating a new carbon management economy. The WBCSD will continue to be at the forefront of these discussions, and we look forward to collaborating with organisations like the Coalition for Negative Emissions.

Claire O’Neill

Managing Director, Climate & Energy, World Business Council for Sustainable Development

Quotes from academia

“CCRC supports the case for negative emissions and values much of the work contained in this report. CCRC are supportive of a wide range of greenhouse gas removal approaches and it is clear that we need to scale-up urgently. In addition to the methods explored in detail in this report we would encourage research into others. For example, more research into restoration of the oceans is needed, and these in turn may provide further opportunities for natural carbon uptake which could be incredibly significant. Furthermore, there are concerns about rising levels of methane in the atmosphere and we need to develop techniques to tackle this. All of the approaches we need will however face similar challenges to those discussed in more detail in this report, and the discussion included in chapters 3 and 4 is most helpful for the overall field of greenhouse gas removal.”

— Dr Shaun Fitzgerald, Director of Research, Centre for Climate Repair, University of Cambridge

“The scale-up of negative emissions is critical to meeting the Paris agreement, alongside widespread decarbonisation. We need a portfolio of solutions because no single approach is likely to be enough and there is huge scope for innovation. Durability is important, too. Net zero requires any removed CO2 to stay locked away from the atmosphere, so we must encourage and invest in solutions that store carbon for as long as possible.”

— Dr Steve Smith, Executive Director, Oxford Net Zero, University of Oxford

Key messages

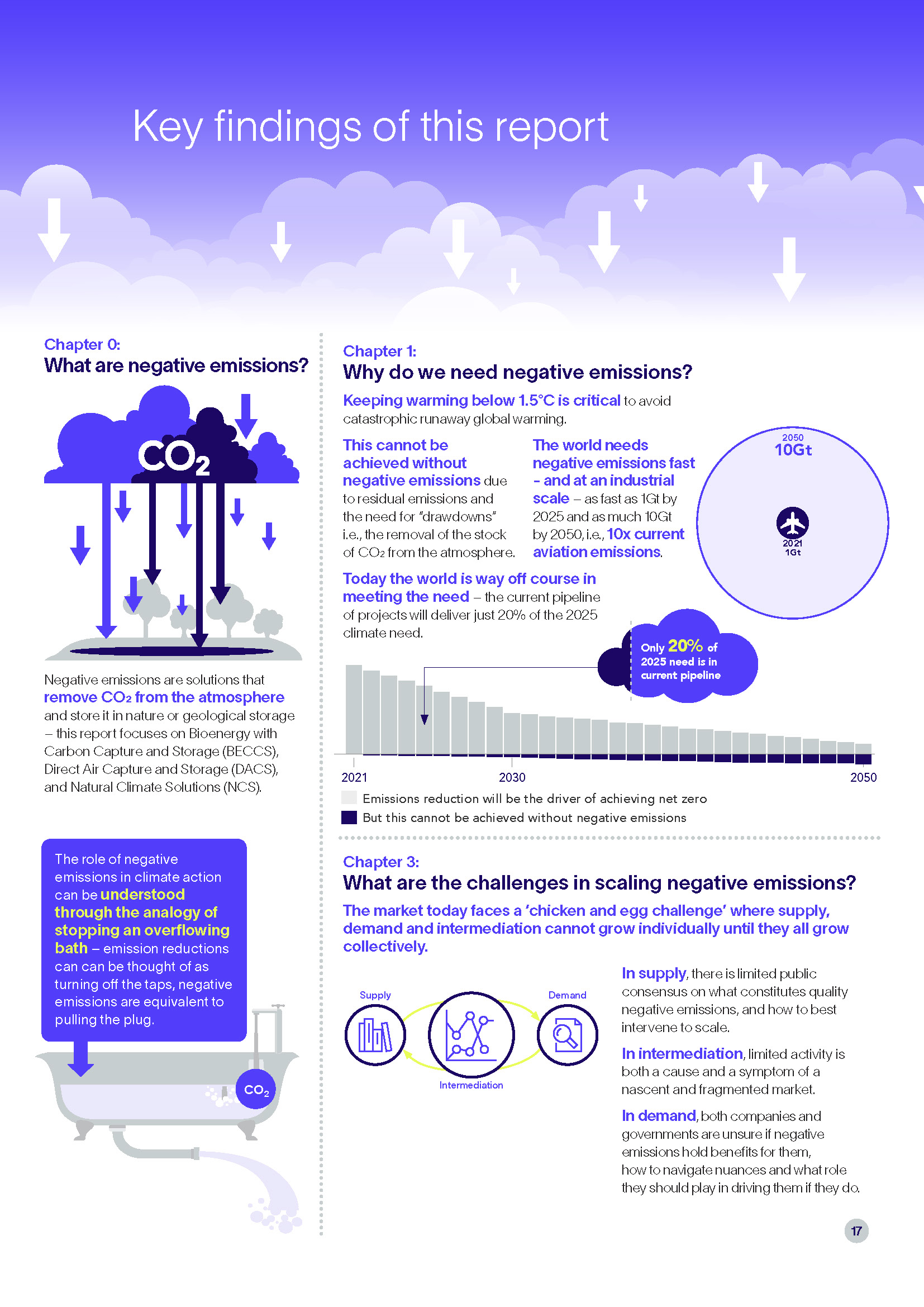

Keeping global warming below 1.5°C is critical to avoid catastrophic runaway climate change.

At present emissions levels, the 1.5°C threshold will be exceeded before 2040. Above 1.5°C, climate feedback loops may lead to permanent runaway climate change.

Keeping warming to 1.5°C cannot be achieved without negative emissions.

Emissions reduction will be the main way to adhere to a 1.5°C pathway, but this alone is not enough. Negative emissions – achieved through solutions that actively remove CO2 from the atmosphere and store it long term – are essential. Negative emissions solutions neutralise residual, hard-to-abate emissions, reduce atmospheric CO2 in the event of overshoots (that is, if emissions reductions are not delivered quickly enough), and remove historic emissions already in the atmosphere. Many negative emissions solutions exist today; examples include bioenergy with carbon capture and storage (BECCS), direct air capture and storage (DACS), and natural climate solutions (NCS) such as reforestation.

Negative emissions cannot be an excuse for slow reductions in emissions.

In an ideal world negative emissions would not be needed at all, however they are in all major 1.5°C pathways as a consequence of the realities of the climate situation the world finds itself in today. Negative emissions work alongside emissions reduction solutions; they are not a substitute and must not detract from efforts to reduce emissions.

Negative emissions solutions are an integral and necessary part of all IPCC 1.5°C pathways and must scale rapidly and to an industrial scale to meet this need.

In pathways that limit warming to 1.5°C, negative emissions scale rapidly in the short term to achieve global removal of 0.5 to 1.2 Gt of CO2 per year by 2025, according to the Intergovernmental Panel on Climate Change (IPCC). Negative emissions must also scale to significant volumes in the medium term, removing as much as 6 to 10 Gt of CO2 globally per year by 2050.

Today, the world is far from a trajectory that will meet the need for negative emissions.

Based on the current pipeline of projects, the negative emissions required by 2025 in the IPCC’s 1.5°C pathway will be missed by 80 per cent. Investment in negative emissions solutions is also lagging and is 30-fold underinvested based on its contribution to a 1.5°C pathway (versus fourfold for emissions reduction solutions).

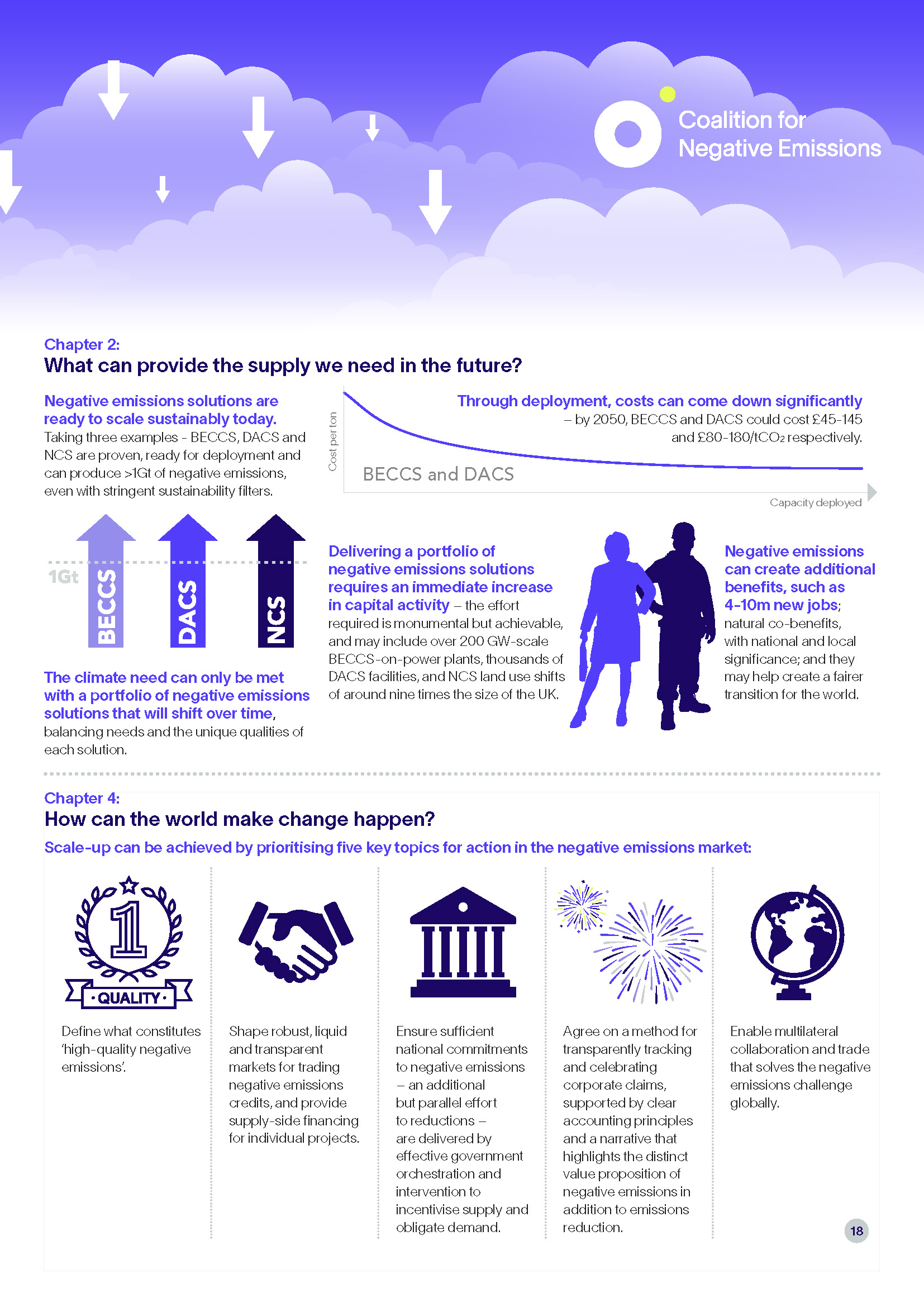

Negative emissions solutions are ready to scale sustainably today.

Taking three examples – BECCS, DACS and NCS are proven, ready for deployment, and can provide 1 Gt or more each of negative emissions, even with stringent sustainability filters (including no land use changes for BECCS). Further negative emissions potential can be generated from other solutions, which can help provide resilience on the path to meeting the 1.5°C pathway need.

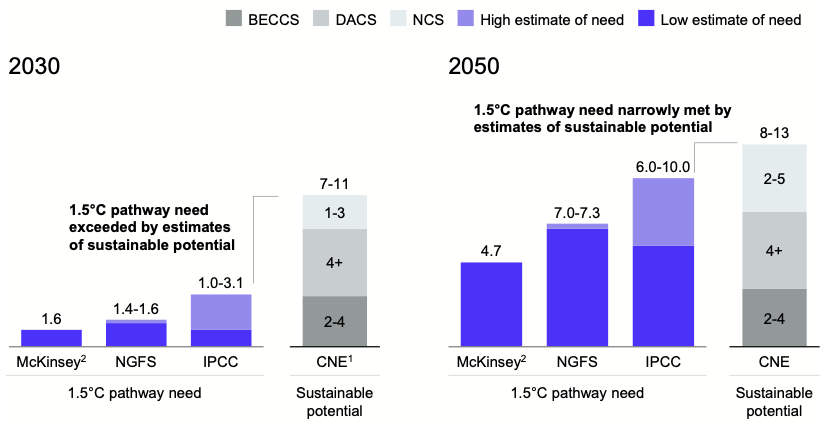

The 1.5°C pathway need can be met with a portfolio of negative emissions solutions.

The IPCC’s 2050 target can only be met with a mix of emissions reduction and negative emissions solutions. Different negative emissions solutions serve different roles and have different characteristics. For example NCS can be deployed rapidly, and have co-benefits beyond the climatic (such as biodiversity and better water quality). Over time, however, the mix will need to include solutions that use long-term storage with a lower risk of reversal (such as geological storage), bringing the benefits of negative emissions production that does not saturate over time and negative emissions that can be stored with a lower risk of reversal. Other solutions (such as those with oceanic storage) will also need to be integrated into the portfolio as they emerge.

Delivering a portfolio of negative emissions solutions requires an immediate increase in capital activity.

Meeting 1.5°C pathway needs could mean, for example building over 200 gigawatt-scale BECCS-on power plants and thousands of DACS facilities, and creating NCS land-use shifts of around ten times the size of the UK. Wider enablers are also critical – including scaling up biomass supply chains, developing project delivery skills, and building out carbon capture and storage (CCS) networks. While this is a vast undertaking, it is technically feasible. However, many negative emissions solutions along with their enabling infrastructure have significant scale-up times, so a 1.5°C pathway can only be achieved if activity and investment in all solutions accelerates rapidly.

Deployment at scale can reduce the cost of negative emissions solutions significantly.

Even at present-day costs, the cost of inaction dwarfs the cost of negative emissions solutions, due to the economic damage that would grow exponentially if warming rises. And the costs of solutions are very likely to fall rapidly with deployment at scale, as has been shown in the scaling of other technologies. using an illustrative portfolio of of BECCS, DACS and NCS, the average negative emissions solution is estimated to cost around £30 to £100 per tonne of CO2 that it eliminates by 2050, once deployed at scale. The expected cost reduction means that deploying such a portfolio sufficient to achieve a 1.5°C pathway will cost £7 trillion to £10 trillion: around £3 trillion to £6 trillion cheaper than present costs imply.

At-scale negative emissions solutions can bring about broader societal benefits.

These include social co-benefits such as the creation of four million to ten million new jobs and effective skills transfers (for example, oil and gas STEM professionals have a 70 to 90 per cent skills match with BECCS and DACS STEM professionals). These can also include other environmental co-benefits, such as biodiversity benefits from carefully planned reforestation or mangroves reducing the threat of storm surges on coastal cities.

Challenges in supply, intermediation and demand need to be resolved simultaneously in order for negative emissions solutions to scale:

- In supply, there is no consensus on what constitutes ‘high-quality negative emissions’. There is a need to answer concerns about the safety and environmental impact of certain solutions without allowing perfection to be the enemy of good in terms of scaling a sustainable portfolio. In addition, the financial landscape is challenging for early suppliers, for example ‘first of a kind’ solutions that need funding to start the cost reduction process do not have easy access to support.

- In intermediation, limited activity is both a cause and a symptom of a nascent and fragmented market. Lack of mature trading infrastructure (such as exchanges, benchmarks and data) deters parties from entering the market to transact an asset that itself has uncertain value. With limited transactions taking place, traders, financiers, lawyers and accountants are not developing adjacent services for the market.

- Finally, in demand, both companies and governments are unsure whether negative emissions solutions hold benefits for them, how to navigate nuances (between solutions, between standards and across a vast range of price points) and what role they should play in driving them.

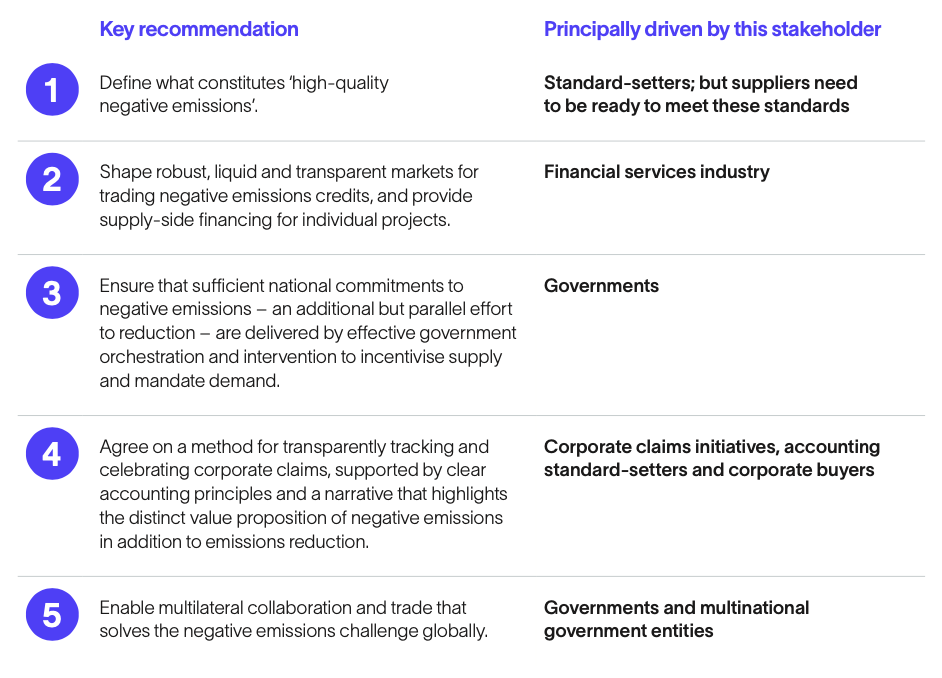

A functioning market for negative emissions solutions can be created through five substantive actions, which are based on early evidence in the emerging negative emissions solutions market and comparable decarbonisation scale-ups:

- Define what constitutes ‘high-quality negative emissions’.

- Shape robust, liquid and transparent markets for trading negative emissions credits, and provide supply-side financing for individual projects.

- Ensure that sufficient national commitments to negative emissions – an additional but parallel effort to emissions reduction – are delivered by effective government orchestration and intervention to incentivise supply and mandate demand.

- Agree on a method for transparently tracking and celebrating corporate claims, supported by clear accounting principles and a narrative that highlights the distinct value proposition of negative emissions in addition to emissions reduction.

- Enable multilateral collaboration and trade that solves the negative emissions challenge globally.

Executive summary

Human activity is destabilising the Earth’s climate. A rise in global average temperatures is already having a significant impact on weather systems and society. Climate science tells us that if global average temperatures rise more than 1.5°C above pre-industrial levels, this impact could become catastrophic and potentially irreversible.

To avoid such devastating impact, action is required now. Emissions reduction will be the main way to adhere to a 1.5°C pathway, but this alone is not enough. Negative emissions – achieved through technologies that actively remove CO2 from the atmosphere and store it long term – are an essential part of the solution. These technologies can neutralise residual, hard-to-abate emissions, draw down any emissions overshoot if emissions reductions are not delivered quickly enough, and remove historic emissions already in the atmosphere.

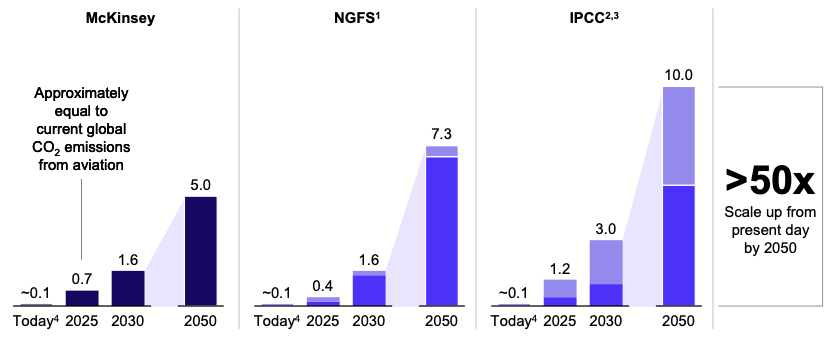

To limit warming to 1.5°C, multiple pathways state that the world needs negative emissions. Each of these pathways makes different assumptions on CO2 reduction and CO2 removals to meet 1.5°C, but all demonstrate that the short-term scale-up should be rapid (reaching around 1 Gt of negative emissions by 2030) and that the long-term need demands massive quantities (reaching around 5 to 10 Gt of negative emissions by 2050) – see Figure 1. Even pathways that rely on more ambitious reduction pathways agree that negative emissions are needed at the gigaton scale. For example the IEA pathway, which features more CCS use and faster reductions in transport and energy, still features around 4Gt of negative emissions by 2050.

Figure 1:

Negative emissions need to scale up rapidly to meet climate targets

Gigatonnes per year of negative emissions required in integrated pathways to 1.5°C

Note: For scenarios with ranges, only the high value is labeled.

- Network for Greening the Financial System.

- Intergovernmental Panel on Climate

- Range of median values for three 5°C warming pathways published by the IPCC (less than 1.5°C, low overshoot, high overshoot).

- Today estimates from Coalition for Negative Emissions Source: IPCC; NGFS; McKinsey

Figure 1 is a synthesis of pathways which limit warming to 1.5°C or 2°C, developed by the Network for Greening the Financial System (NGFS), the Intergovernmental Panel on Climate Change (IPCC), and McKinsey. The y-axis shows the need in gigatonnes according to the different sources in different years, shown along the x-axis. Pathways like the IPCC’s are based on the results of integrated assessment models which take different academic fields (such as climate, energy systems, and economic models) and link them in ‘integrated’ models to yield more insight, rather than evaluating different academic fields in silos. For example, the climate component of an integrated assessment model might impact the socioeco- nomic development of a society, which impacts the emissions trajectory, which in turn impacts the climate component of the model [Special report: Global warming of 5°C, IPCC, 2018, www.ipcc.ch/sr15/.]

If negative emissions solutions are not scaled, even if all 1.5°C emissions reduction pathway requirements are met, the world will break the carbon budget and exceed 1.5°C warming before 2040.

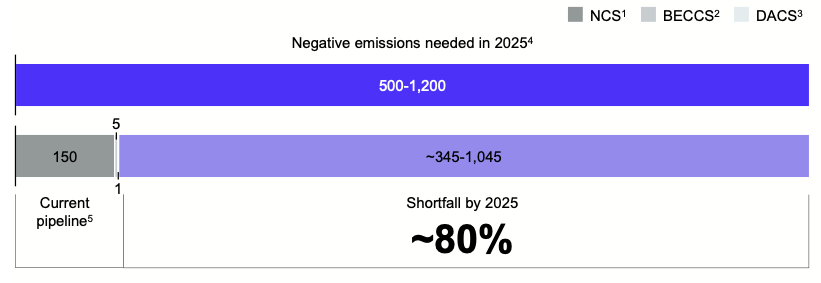

Despite a clear and present need, action on negative emissions is falling dramatically short of what will be required. Projections based on the current engineered emissions removal pipeline and historic reforestation rates suggest that the 2025 target will be missed by more than 80 per cent (see Figure 2). [The shortfall was calculated by scanning press releases for all BECCS and DACS plants currently being planned or already in operation, and assuming that all of these are built by Reforestation is assumed to occur at the same, current rate for each year between now and 2025.]

Investment tells a similar story: while all decarbonisation investments currently fall short of what is required, negative emissions solutions are disproportionately underinvested – at around one-thirtieth of the level that would be expected if funding followed the climate need identified in the IPCC’s 1.5°C pathway.

Figure 2:

The pipeline of negative emissions solutions is insufficient to achieve the required 2025 levels of negative emissions

Fully operational 2025 negative emissions capacity implied by current pipeline

Negative emissions required in 1.5°C warming pathways vs. current pipeline, megaton CO2

- Natural Climate

- Bioenergy with Carbon Capture and

- Direct Air Capture and

- Value shown represents the average of the median values for three 5°C warming pathways published by the Intergovernmental Panel on Climate Change (less than 1.5°C, low overshoot, high overshoot).

- The estimated current pipeline of negative emissions refects the long lead times for BECCS and DACS projects and the historic run rates for NCS The BECCS pipeline estimate is based on projects recorded by CCS Institute; the DACS estimate is based on the publicly-stated pipelines of Carbon Engineering, Climeworks, and Global Thermostat, which are the 3 largest DACS producers; and the estimated pipeline for NCS accounts for historical activity rates (~3 Mha per year between 2010-2030 & average carbon removals of ~10t/Ha) & a conservative assumption of 5 full years to 2025.

Source: Carbon Engineering; CCS Institute; Climeworks; FAO; IPCC; McKinsey

Globally, approximately 650 Mt of additional negative emissions capacity needs to be set in motion by the end of 2021 – four times the current pipeline – to meet the IPCC’s average 2025 target. If this is not met, the world will continue on a dangerous trajectory towards irreversible warming.

The longer the need is not addressed, the harder it will be to course correct. If there is no action until 2025, catching up by 2030 will take twice the effort. For example, if the negative emissions need was met entirely by NCS: instead of reforesting an area half the size of the UK each year, the world would need to annually reforest an area the size of the whole UK. Eventually, catching up becomes unfeasible. If there is no action until 2030, around 8 Gt

of negative emissions debt will have been accrued – illustratively, the EU would need to jump more than two years ahead on its reduction plan to keep the world within the carbon budget. Attempting to compensate by pursuing even faster emissions reduction than already mandated in a 1.5°C pathway could increase socioeconomic disruption of the transition, and be challenged by the need to address residual emissions for which no technical answer exists today.

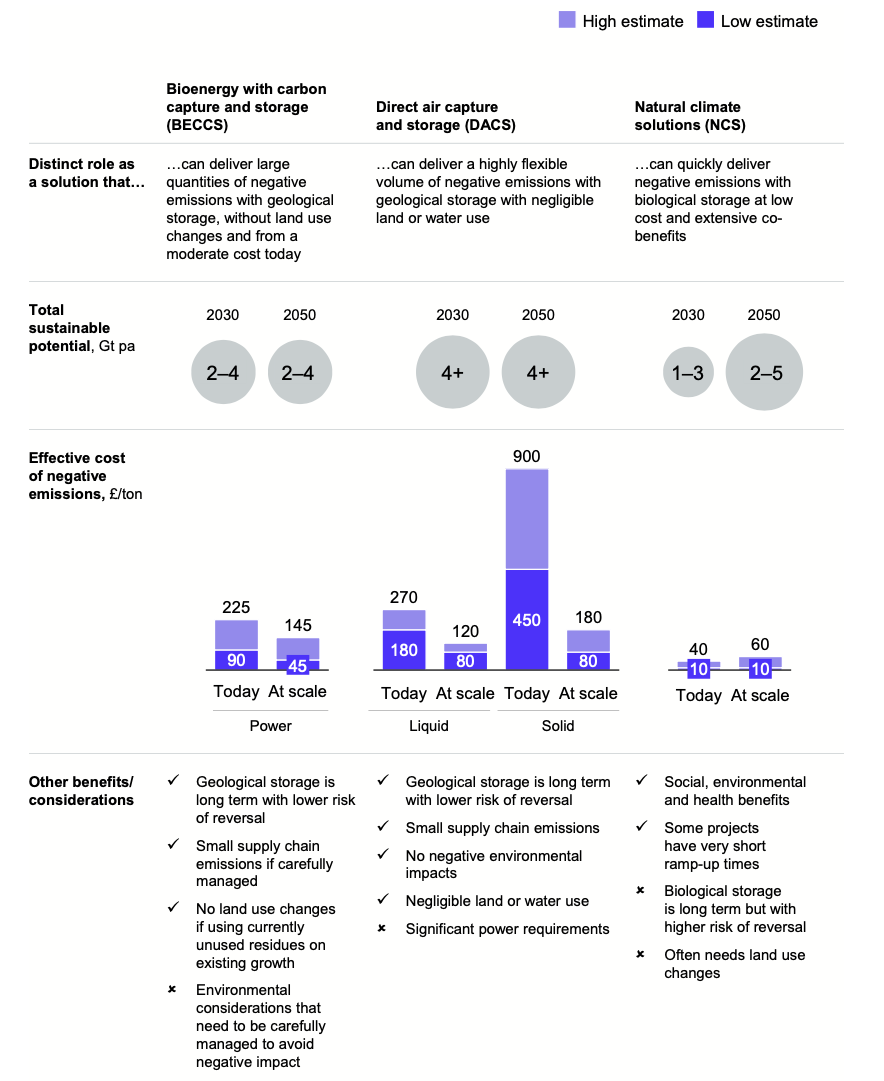

The required solutions for at least the near-term negative emissions do exist today, however. This report explores three major solutions (see Figure 3) and finds that – in combination – these could provide the necessary supplyat least up to 2050 (see Figure 5). The three solutions are: bioenergy with carbon capture and storage (BECCS, be it on power, industry or fuel), direct air capture and storage (DACS) and natural climate solutions (NCS). Each could be sustainably scaled up for gigatonnes of production. This is based on advanced geospatial modelling drawing on over 15 data layers, interviews with over 50 leading land-use experts and hundreds of peer-reviewed academic publications. It is very likely that other solutions will also scale to make material contributions to negative emissions need. So, whilst a combination of BECCS, DACS and NCS may not be the optimal suite of options for all situations over the next 30 years, this does represent a viable and realizable pathway.

Figure 3:

Different solutions have a unique role to play in delivering negative emissions

Example: BECCS, DACS and NCS

- Effective cost subtracts non- CO2 outputs, e.g., wood for certain NCS, power for BECCS on power.

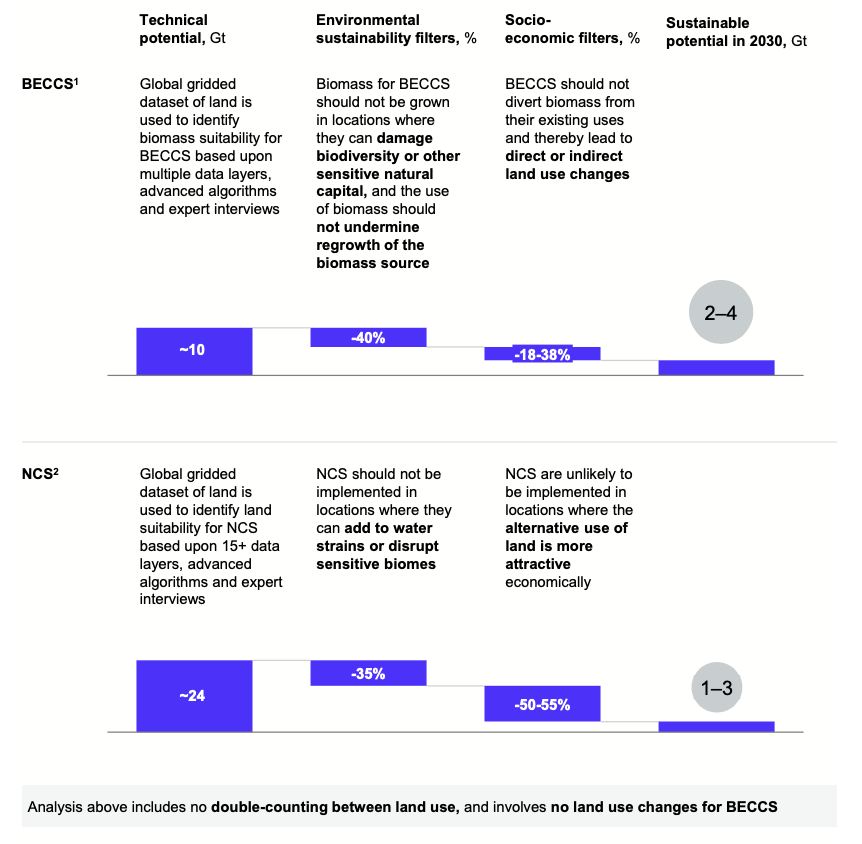

It is critical that the solutions used to produce negative emissions are environmentally and economically sustainable. For example, environmentally, they must not destroy existing carbon stores or damage sensitive ecosystems. Similarly, economically, if they cause disruptions to other value chains or detract from land uses like food production, it is unlikely they will stand the test of time. Consequently, the production potential quoted in this report takes into account stringent economic and environmental sustainability filters, including on land use (BECCS and NCS illustrated in Figure 4), to create sustainable potential for each negative emissions solution.

Figure 4:

Even with stringent sustainability filters, BECCS and NCS can still provide gigatonne-scale negative emissions by 2030

Example: BECCS and DACS in 2030

- Based on agricultural residues, woody residues, and energy crops only on degraded

- Based on wetland restoration (seagrass and mangroves), reforestation, cover crops, trees in croplands and natural forest

Source: McKinsey Nature Analytics

A portfolio approach is likely the only way to meet the negative emissions need as none of the examined solutions can meet the 1.5°C pathway need individually. The focus solutions of this report, BECCS, DACS and NCS, can just meet the 2050 need in combination (see Figure 5). Many other negative emission solutions should be integrated in to the portfolio to help meet the need.

The portfolio of solutions needs to deliver rapid impact in the short term, create substantial capacity in the medium term, and ensure continuity and permanence (that is, a low risk of reversal) in the long term. As a result, the portfolio focus should shift over time from solutions involving solutions with a high risk of reversal (for example, those that store CO2 in plants) to include those with a low risk of reversal (for example, those that store CO2 sealed rock formations underground).

Figure 5:

A combination of existing solutions can theoretically fulfil the climate need through to 2050 but no approach can do it alone and more options are needed to provide resilience and future capacity

- Coalition of Negative Emissions

- McKinsey value represents average

Source: Range of median values of three IPCC 1.5 degree pathways, IPCC less than 1.5 degrees, IPCC 1.5 low overshoot, IPCC 1.5 high overshoot; McKinsey Nature Analytics

The supply of negative emissions can be scaled to deliver this portfolio. However, it will require a monumental shift in investment and an increase in activity (for example, building 200-GW-scale BECCS plants and thousands of DACS facilities, and achieving NCS land-use shifts of around ten times the size of the UK), as well as collaboration between multiple parties to put critical enablers in place (such as sustainable biomass supply chains, project delivery skills and CCS networks). Given that our examples of BECCS, DACS and NCS, along with their enabling infrastructure, have significant scale-up times, this acceleration needs to start today.

Even at present-day costs, the cost of inaction dwarfs the cost of investing to scale negative emissions solutions to meet 1.5°C pathway needs. This is because not meeting the negative emissions need in a 1.5°C pathway will

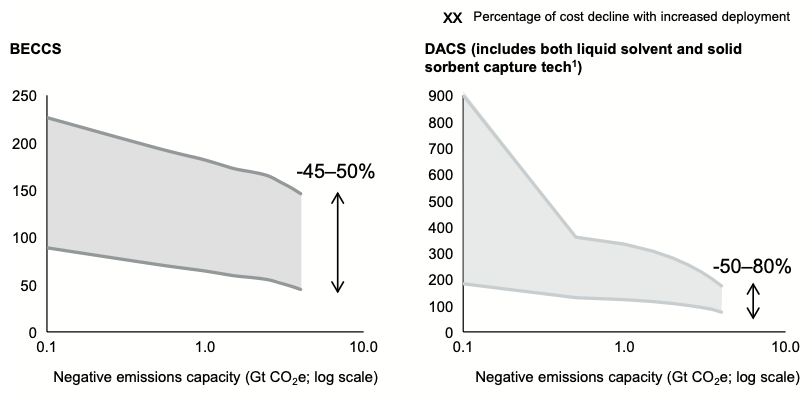

lead to an increase in world temperatures. This in turn will cause climatic risk to grow exponentially; for example, the frequency of extreme rainfall events is predicted to more than double in a world with 2°C of warming versus 1.5°C. The costs of delivering a portfolio is likely to also cost less than today’s perspective implies. Historical comparisons are relevant, for example, the cost of lithium batteries fell more than 85 per cent between 2010 and 2018 as their deployment increased dramatically. Every time cumulative deployment doubled, the cost of these batteries fell around 18 per cent, an effect known as the learning curve. [Logan Goldie-Scot ‘A Behind the Scenes Take on Lithium-ion Battery Prices’, BloombergNEF, March 2019.] Factoring in cost reductions achieved by estimated learning curves, the negative emissions portfolio is estimated to come at a cost of £7 trillion to £10 trillion, which is £3 trillion to £6 trillion less expensive than present-day costs suggest. History has shown that scaling immature technologies reduces their cost, suggesting that solutions with geological storage – including BECCS and DACS – will come down in cost when deployed at the scale needed (see Figure 6). By 2050, the average negative emissions solution is likely to cost £30 to £100 per tonne of negative emissions, given appropriate investment.

Figure 6:

Some negative emissions solutions will decrease in cost as they are scaled

Example: BECCS and DACS

£/ton CO2 negative emissions, low to high ranges

Note: NCS stays broadly low cost over scale. There are some increases in cost towards the upper ends of its technical potential as you move from cheaper to more expensive projects; land prices may also rise with time. In contrast there are savings around streamlined assessment process. See the NCS deep dive for more details.

- Today, liquid is at the lower end of the cost range, solid is at the higher

Source: Coalition for Negative Emissions analysis

Figure 6 shows a forecast of the cost of sequestration for 1 t of CO2 on the y-axis, and the scale of deployed capacity on the x axis. The x-axis is shown in logarithmic terms, as scaling effects are non-linear in general terms. As solutions with geological storage scale-up, their costs come down due to improvements through learning curves (such as process and manufacturing optimisation). The range of cost estimates also shrinks due to several effects, including that some costs have a multiplicative relationship with others (such as financing costs on capital).

At present, the scale-up of negative emissions solutions is hampered by shortcomings in supply, intermediation and demand that disincentivise action.

- In supply, there is no consensus on what constitutes ‘high-quality negative emissions’. There is a need to answer concerns about the safety and environmental impact of certain solutions without allowing perfection to be the enemy of good in terms of scaling a sustainable In addition, the financial landscape is challenging for early suppliers, for example ‘first of a kind’ solutions that need funding to start the cost reduction process do not have easy access to support.

- In intermediation, limited activity is both a cause and a symptom of a nascent and fragmented market. Lack of a mature trading infrastructure (such as exchanges, benchmarks and data) deters parties from entering the market to With limited transactions taking place, traders, financiers, lawyers and accountants are not developing adjacent services for the market; nor are there easily available options for suppliers to access project funding.

- Finally, in demand, both companies and governments are unsure whether negative emissions solutions hold benefits for them, how to navigate nuances (between solutions, between standards and across vast price points) and what role they should play in driving these solutions.

Five substantive actions emerge from the examination of these challenges and from evidence from initial interventions in the emerging negative emissions solutions market and other comparable decarbonisation scale-ups. To create a functioning negative emissions solutions market capable of scaling currently deployable negative emissions solutions to the volumes required, stakeholders should prioritise the following:

If prioritised by stakeholders, these actions can help scale negative emissions solutions to meet the 1.5°C pathway need. Although this will not be easy or immediate, confidence can be drawn from both successful interventions

in comparable contexts. Early momentum is already evident in the negative emissions market – intermediaries in voluntary markets are acknowledging their need to step-up, a number of companies have emerged as negative emission front-runners and country domestic plans are showing greater and greater ambition on negative emissions. This momentum can be capitalised upon to unlock the market.

The world is currently not on track to deliver enough negative emissions to achieve the 1.5°C pathway need. There is still time to perform a dramatic course correction and establish a vibrant and sustainable negative emissions solutions market that delivers a sustainable portfolio of negative emissions supply. But action has to start today.

About the Coalition for Negative Emissions

We believe in a net-zero future, and we have the scale and expertise to help create it.

Our current members include landowners and environmental stewards, large users and generators of energy, technology start-ups and large manufacturers and operators within aviation and agriculture.

We represent a substantive part of the negative emissions supply chain. For example, in the supply of negative emissions we feature two of the world’s three most prominent DACS companies, the UK’s largest representative group for agricultural landowners and the company behind the world’s largest planned BECCS project. In demand we feature the first airline group worldwide to commit to net-zero emissions, and the world’s second-busiest airport in terms of international passengers. [Civil Aviation Authority; https://www.co.uk/Data-and-analysis/UK-aviation-market/Airports/Datasets/. ]

This commercial insight is complemented by influential trade and groups, such as the UK’s leading business organisation, representing 190,000 businesses, and the world’s largest CCS organisation.

Given our breadth of expertise, we have unique insight into the scale of the challenges faced in reaching climate targets. We also have expertise in how to address those challenges in a manner that will allow economies and sustainable industries to thrive.

We have a shared ambition: to create a sustainable economy while helping protect the environment. Our goal is not just to decarbonise, but to decarbonise while ensuring continued economic progress. To do this, negative emissions will be essential.

We welcome new members with an interest in the negative emissions supply chain to join the Coalition for Negative Emissions, wherever in the world they plan to drive the scale-up.

And, we have an open attitude to partnership. As the Coalition for Negative Emissions grows, so does our reach and depth of expertise. However, no matter how large we grow, we are always intentionally inclusive of other groups, actively co-creating research and sharing learning with those with related interests.

Agricarbon is a UK-based disruptive technology start-up commercialising a low-cost, scalable solution for highly accurate DIRECT measurement of soil carbon stock (SOC) in farming and natural landscapes. Agricarbon is unique in addressing the industry-wide need for affordable, accurate, independently assessed and future-proofed SOC data (‘ground-truth’ data) at scale. This underpins the growth in precision farming and agricultural carbon removals markets with robust, decision-grade evidence, and supports the decarbonisation of food and farming supply chains. Soft-launched in the UK, in 2021 Agricarbon will provide a robust, directly measured soil carbon baseline for over 40,000 acres of farmland on behalf of First Milk co-operative and Nestle. Our aim is to scale quickly and establish Agricarbon as a global standard for high integrity quantification and certification of soil carbon stock and unlock the huge potential for carbon capture and storage in soils.

Association for Renewable Energy & Clean Technologies (REA) is the largest renewable energy and associated clean technology trade body in the UK, with around 500 member organisations representing stakeholders from across the heat, power, circular bioresources and transport sectors. Our members include generators, project developers, fuel and power suppliers, investors, equipment producers and service providers. This includes members at the forefront of delivering carbon capture and storage solutions across a range of bioenergy technologies, as well those involved in organic recycling and cultivation of bioenergy feedstocks, delivering further natural carbon solutions. The REA supports and advocates for the development of these greenhouse gas removal technologies, recognising their critical importance in achieving the UK’s net-zero ambitions.

At Bank of America, we’re guided by a common purpose to help make financial lives better, through the power of every connection. We’re delivering on this through responsible growth with a focus on our environmental, social and governance (ESG) leadership. ESG is embedded across our eight lines of business and reflects how we help fuel the global economy, build trust and credibility, and represent a company that people want to work for, invest in and do business with. It’s demonstrated in the inclusive and supportive workplace we create for our employees, the responsible products and services we offer our clients, and the impact we make around the world in helping local economies thrive. An important part of this work is forming strong partnerships with nonprofits and advocacy groups, such as community, consumer and environmental organizations, to bring together our collective networks and expertise to achieve greater impact. In 2021 Bank of America announced its commitment to achieve Net Zero before 2050 and in 2019 announced it had achieved carbon neutrality, a year ahead of schedule. It also announced a sustainable finance commitment of $1.5 trillion by 2030, of which $1 trillion is dedicated to environmental transition as part of its Environmental Business Initiative (EBI). The company’s EBI has already deployed more than $200 billion to low-carbon, sustainable business activities since 2007.

Biomass UK is the subsection of the Association for Renewable Energy and Clean Technology (REA) which focuses on biomass power. It represents nearly 200 owners, operators, suppliers, contractors and investors in the UK’s international biomass supply chain. Biomass UK works with government, politicians, media, academics and others in order to promote a better understanding of biomass energy and its benefits to the UK, including its potential to deliver negative emissions at scale through Bioenergy with Carbon Capture and Storage (BECCS).

The Centre for Climate Repair at Cambridge (CCRC) is a mission-focussed organisation which aims to achieve ambitious action on climate repair, supported by scientific research and robust evidence. Its strategic objectives are to (i) support deep and rapid greenhouse gas emissions reduction (ii) remove greenhouse gases from the atmosphere and (iii) restore parts of the climate system that already pose risks to humanity. The CCRC is working with policy makers in the UK and across the globe to build alliances of nations and states dedicated to meaningful carbon sequestration solutions and technologies to safeguard our planet. In addition, CCRC is collaborating with sister Universities around the globe to both expand the scale of research efforts and policy discussions, and engaging with the public and other stakeholders to progress action to tackle climate change.

The Carbon Capture and Storage Association (CCSA) is a trade association, set up to represent the interests of its members in promoting the business of capture and geological storage of carbon dioxide (known as Carbon Capture, Utilisation and Storage, or CCUS) as a means of abating atmospheric emissions of carbon dioxide. The CCSA works to raise awareness of the essential role that CCUS will play in delivering net- zero emissions across industry, heat, transport and power – as well as unlocking a key method of greenhouse gas removal through sustainable bioenergy with CCS (BECCS) and Direct Air Capture with Storage (DACS). To this end, the Association works with the UK Government and European Commission, and engages in international processes, to develop appropriate regulations and incentive mechanisms that will deliver the necessary commercial-scale CCUS projects to achieve climate goals.

Carbon Engineering is deploying Direct Air Capture (DAC) technology at megatonne scale. Captured atmospheric CO2 can then be safely and securely stored underground offshore or converted into sustainable transport fuels and other products. One plant does the work of around 40 million trees but with significantly less water and land use and removals are permanent, measurable and verifiable. The regenerative process uses standard industrial equipment assembled on site meaning plants can be rapidly deployed and a full local supply chain is developed. In the US the world’s largest DACS facility using Carbon Engineering’s technology is due online in 2024. In the UK, Carbon Engineering and Storegga plan to deploy a commercial DACS facility in North East Scotland. Construction could begin in 2024 and the plant could be operational by 2026.

The CBI speaks on behalf of 190,000 businesses of all sizes and sectors across the UK. The CBI’s corporate members together employ nearly 7 million people, about one third of private sector-employees. Business is at the heart of delivering the UK’s net-zero target, with firms delivering and adopting the negative emissions technologies and solutions integral for achieving it.

Climeworks empowers people to reverse climate change by permanently removing carbon dioxide from the air. One of two things happens to the Climeworks air-captured carbon dioxide: either it is returned to earth, stored safely and permanently away for millions of years, or it is upcycled into climate-friendly products such as carbon- neutral fuels and materials. The Climeworks direct air capture technology runs exclusively on clean energy, and the modular CO2 collectors can be stacked to build machines of any size. Climeworks is currently constructing the world’s first large-scale direct air capture and storage plant “Orca”. Orca will take carbon dioxide removal to the next level by capturing 4000 tons of CO2 per year. Founded by engineers Christoph Gebald and Jan Wurzbacher, Climeworks strives to inspire 1 billion people to act now and remove carbon dioxide from the air.

Confor is a members’ organisation that represents the sustainable forestry and wood products industry across the UK. Planting trees is a nature based means to sequester carbon and that can then be locked up in wood products.

Drax Group is a UK-based renewable energy company engaged in renewable power generation, the production of sustainable biomass and the sale of renewable electricity to businesses. It is the UK’s largest source of renewable electricity. Enabling a zero carbon, lower cost energy future is Drax Group’s purpose and in 2019, it announced a world-leading ambition to be carbon negative by 2030, using Bioenergy with Carbon Capture and Storage (BECCS) technology to remove carbon dioxide from the atmosphere at scale whilst delivering reliable renewable electricity. Work to build BECCS could get underway at Drax Power Station as soon as 2024, and by 2027 Drax’s first BECCS unit could be operational, delivering the UK’s largest carbon capture project and permanently removing millions of tonnes of carbon dioxide from the atmosphere each year.

Energy UK is the trade association for the energy industry with over 100 members spanning every aspect of the energy sector – from established FTSE 100 companies, right through to new, growing suppliers and generators, which now make up over half of our membership. We represent the diverse nature of the UK’s energy industry with our members delivering over 80% of both the UK’s power generation and energy supply for the 28 million UK homes as well as businesses. The energy industry invests £13bn annually, delivers £31bn in gross value added on top of the £95bn in economic activity through its supply chain and interaction with other sectors, and supports 738,000 jobs in every corner of the country.

Enviva is the world’s largest producer of industrial wood pellets, a renewable and sustainable energy source used to generate electricity and heat. We export our pellets to energy generators in the United Kingdom, Europe, and Japan that previously were fueled by coal, enabling them to reduce their lifecycle carbon footprint by more than 85 percent. Enviva’s mission is to displace coal, grow more trees, and fight climate change. Since inception, the company has displaced 16 million metric tons of coal, recorded a cumulative 400 million-metric ton increase in forest inventory across its sourcing regions in the US Southeast, and avoided a cumulative 31 million metric tons of CO2 emissions. We make our pellets using sustainable practices that protect US Southern forests and create a market for sustainable low-value wood that encourages good forest stewardship and creates incentives for forest landowners to replant and keep their land as forest.

Heathrow Airport has been at the forefront of advocacy and change on reducing carbon emissions in the aviation sector. At the start of 2020, UK aviation became the first national aviation sector in the world to commit to net zero by 2050, with Heathrow playing a key role. Heathrow believes that well-designed policy for negative emissions, and a rapid scaling up of solutions, will play a significant role in delivering net zero during this decade and beyond.

International Airlines Group (IAG) is one of the world’s largest airline groups, with leading airlines in Spain, the UK and Ireland. Before the impact of the COVID-19 pandemic, IAG operated to 279 destinations and carried around 118 million passengers each year. In 2019 IAG became the first airline group in the world to commit to achieving net zero emissions by 2050 and to publish a clear roadmap to deliver this. Recognised by the UN as one of 10 global companies for its bold climate targets, IAG’s ambition is to be the world’s leading airline group on sustainability. That means using its scale, influence and track record to not only transform its business, but drive the system-wide change required to create a truly sustainable aviation industry. As part of collaborating on the breakthroughs it needs to achieve its ambitious targets, IAG is offsetting carbon as a transitional step and supporting the development of negative emissions solutions over the long term.

MGT Teesside Limited is a new biomass CHP generation plant nearing completion in Teesside. It is part of the Teesside carbon cluster working alongside cluster members to achieve net zero in line with government targets and also playing a significant part in the development of the green economy, both nationally and regionally in the north-east.

The Mineral Products Association (MPA) is the trade association for the aggregates, asphalt, cement, concrete, dimension stone, lime, mortar and silica sand industries. Industry production represents the largest materials flow in the UK economy and is also one of the largest manufacturing sectors. There are a wide range of opportunities for mineral products to removeCO2 from the atmosphere both in their production, such as through the use of waste biomass fuels with CCUS (industrial BECCS) in cement manufacture or the use of gaseous biofuels and CCUS in lime manufacture, and through the use of mineral products in applications such as Direct Air Capture Systems and enhanced weathering. These removals could contribute significantly to the UK’s net zero ambition, for example, industrial BECCS has the potential to remove almost 2 million tonnes of CO2 from the atmosphere every year.

The National Farmers Union of England and Wales (NFU) champions British agriculture and horticulture, to campaign for a stable and sustainable future for our farmers and growers. The NFU is pleased to be working alongside other industries, contributing to world-leading greenhouse gas removal plans as part of our 2040 Net Zero ambition for the agricultural sector. We believe that the many forms of biomass production offer a critically important opportunity for agriculture and the land-based sector to demonstrate our capability to capture carbon dioxide through photosynthesis and couple it to a variety of carbon capture and storage technologies.

Natural Capital Partners have more than 300 clients in 34 countries and are harnessing the power of business to create a more sustainable world. Through a global network of projects, the company delivers the highest quality solutions which make real change possible: reducing carbon emissions, generating renewable energy, building resilience in supply chains, conserving and restoring forests and biodiversity, and improving health and livelihoods. We welcome the focus that the Coalition for Negative Emissions brings to the critical importance of removals in the expanding portfolio of climate mitigation solutions.

Petrofac is a leading international service provider to the energy industry and our purpose is to enable our clients to meet the world’s evolving energy needs. We have been designing, building, managing, operating, and maintaining infrastructure for clients across the energy sector for 40 years and have delivered projects across the Middle East, North Africa, UK, Australia, India, South East Asia, and the United States. Our track-record for safe and reliable delivery is underpinned by cost- effective, innovative, and tailored delivery models that focus on driving in-country value. Our services span the asset lifecycle, from concept design, specialist consultancy, technology selection and front-end engineering to engineering, procurement, construction, commissioning, operations, maintenance, decommissioning, and training. We support energy infrastructure projects across the offshore wind, hydrogen, carbon capture, utilisation & storage (CCUS) and waste to value sectors, deploying our engineering, project management and operations expertise to safely and efficiently deliver and operate the projects that will get us to Net Zero.

Severn Trent Water is a FTSE100 company providing water and waste water services to more than 4.6 million households and businesses in the England and Wales. We also develop renewable energy solutions. We are determined to play a leading role in addressing the impact of climate change and mitigating our own impact, the impact of our supply chain and adapting to the challenges that climate change may bring in the future. In 2019 we announced our Triple Carbon Pledge – committing to net-zero operational carbon emissions, 100% renewable energy and an all-electric fleet by 2030, subject to the availability of vehicles. In March 2021, we submitted our proposed Scope 1, 2 and 3 emissions targets to the Science Based Targets initiative, committing us to significantly reduce our greenhouse gas emissions by 2030. We recognise that carbon removal is likely to be required in future and that developing negative emissions technologies is essential. We are exploring some of these options ourselves but it is clear that big changes in policy, technology and markets are needed to make these widely deployable.

Storegga is an independent, UK-based carbon management business at the forefront of the global Net Zero strategy. It aims to champion and deliver carbon capture and storage (“CCS”), hydrogen, and other subsurface renewable projects in the UK and internationally to accelerate carbon emission reductions.Through its wholly owned subsidiary, Pale Blue Dot, Storegga is the lead developer of the Acorn Carbon Capture and Storage (“CCS”) and Hydrogen project, providing essential infrastructure to help the UK meet its net zero targets. The Acorn Project will provide critical backbone infrastructure for the Scottish Cluster. The Scottish Cluster unites communities, industries and businesses to deliver CCS, hydrogen and other low carbon technologies, supporting Scotland, the UK and Europe to meet net zero goals. Storegga has joined with leading engineering and technology groups at the forefront of their fields to accelerate infrastructure development. The Company has partnered with Carbon Engineering to develop Direct Air Capture (“DAC”) in the UK. Planning for a commercial DAC plant in North East Scotland linked to the Acorn offshore storage facility is currently in pre-feed. It is anticipated that construction could begin in 2024 with the plant being operational by 2025.

USIPA is a not-for-profit trade association formed in 2011 to promote sustainability and safety practices within the US wood energy industry. We advocate for the wood energy sector as a smart solution to climate change, including delivering negative emissions power generation through Bioenergy with Carbon Capture and Storage (BECCS) technology, and we support renewable energy policy development around the globe. Our members represent all aspects of the wood pellet export industry, including pellet producers, traders, equipment manufacturers, bulk shippers, and service providers.

Velocys is an international UK-based sustainable fuels technology company. Velocys designed, developed and now licenses proprietary Fischer-Tropsch technology for the generation of clean, low carbon, synthetic drop-in aviation and road transport fuel from municipal solid waste and residual woody biomass. The company is at present developing two reference projects: one in Natchez, Mississippi, USA (incorporating Carbon Capture, Utilisation and Storage) and one in Immingham, UK, to produce fuels that significantly reduce both greenhouse gas emissions and key exhaust pollutants for aviation and road transport.

Viridor is one of the UK’s largest recycling and waste management companies. Viridor operates the largest fleet of waste processing facilities that take non-recycled waste and convert it into heat and power. Viridor has a target to be a net zero emissions business by 2040 and climate positive, removing more emissions than we generate by 2045. Negative emissions from Carbon Capture use and storage are a key tool to enable Viridor to reach this ambition. Viridor has already started investigating CCS at its Runcorn facility and has plans to roll this out further. As part of our decarbonisation ambition. Viridor has signed up to the most ambitious goals in the Science Based Target Initiative.

Additional thanks

The Coalition would like to thank Microsoft for co-creating a case study on their activities around becoming carbon negative, as featured in Chapter 4.

Share

View/Download PDF